By Kristen Fountain/VTDigger

Thousands more Vermonters are poised to become eligible for health insurance savings this year after two recent changes to federal guidelines.

For six more weeks, it is open enrollment season for Vermont Health Connect, the state health insurance marketplace and the gateway to federal health insurance subsidies.

Just over 25,000 Vermonters get their insurance through the marketplace, which is operated by the Department of Vermont Health Access, according to the latest available figures. But both the state officials that run it and the insurance companies that sell their products on it think that more people should be buying their health insurance there. They are pushing right now to get the word out about recent changes.

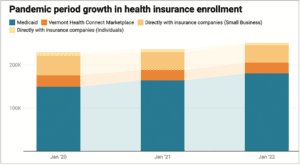

Chart shows more Vermonters are enrolled in a health insurance plan since January 2020 before the pandemic started.

Around 5,360 Vermonters still buy insurance directly through providers such as Blue Cross Blue Shield of Vermont and MVP, according to the latest figures. Eligibility for subsidies was expanded to higher income brackets during the pandemic. That expansion will now be in effect through at least the end of 2025, but not everyone knows this.

This year, Blue Cross is making all re-enrolling customers confirm, either verbally on the phone or by checking a box on a form, that they are not eligible for the federal subsidies available through Vermont Health Connect.

“It was a way to get people to pay attention,” said Sara Teachout, director of government and media relations at Blue Cross Blue Shield of Vermont. “We want to do everything we can to help people get the benefits they qualify for and deserve to have.”

The company is also doing outreach, trying to let employers know about an even more recent change in federal regulations that could save employees’ families thousands of dollars annually on health insurance.

The regulatory change means many more of Vermont’s working families will qualify in 2023 for reduced cost insurance, but only if it is purchased through the marketplace rather than directly through a family member’s employer. One estimate suggests around 14,000 Vermonters are newly eligible.

The deadline to enroll in the marketplace is Jan. 15, but people need to sign up by Dec. 15 for coverage to begin at the beginning of 2023.

Since 2014, when subsidies began, families in which one person has access to employer-based health insurance have been blocked from accessing it, even if the employer does not contribute enough to make insurance for the whole family affordable.

This nationwide problem, which policymakers advocating for the change call “the family glitch,” has finally been resolved. Starting this enrollment period, family members of covered employees living in Vermont are now eligible to purchase insurance through Vermont Health Connect, and receive income-based subsidies, if they are not already covered by other federal health insurance programs such as Medicaid or Medicare.

Adaline Strumolo, deputy commissioner at the Department of Vermont Health Access, said this change, along with the expanded income eligibility, should make health insurance more affordable for thousands more of Vermont’s working families.

“We think it brings the full promise of the Affordable Care Act to life in a way which we just couldn’t do before,” she said.

Strumolo hopes anyone in the state who wishes they paid less for private health insurance will visit the state website again in the next few weeks to check their eligibility for enrollment and subsidies, even if they may have already looked in previous years.

Navigating the site is easier than before, with online tools and in-person consultations available with department staff or trained “assisters” at health clinics across the state. “We would really love for everyone to look again,” Strumolo said.

What is new?

Not Vermont Health Connect, which has been operating for almost a decade. Vermont is one of 18 states that runs its own health insurance marketplace for consumers and small businesses under rules set out by the 2010 Affordable Care Act. Residents of states that don’t operate their own marketplace purchase through a federally run website.

Expanded subsidies, too, have already been established. The 2021 American Rescue Plan Act increased the amount of subsidy available through the program for households already receiving it — those making less than 400% of the federalpoverty rate, which in 2023 is $54,000 for one person or $111,000 for a family of four, for example.

The pandemic recovery law also extended an Affordable Care Act framework that limits the cost of a basic (Silver-level) health care plan to 8.5% of one’s annual household income to all income levels. As a result, there is a subsidy — a small amount at the top range — available at a much higher income range, with the top level being households of three or more people making up to $330,000.

But what is new is that in August, as part of the Inflation Reduction Act, Congress extended those enhanced subsidies for three more years, through the end of 2025. State officials hope this assurance of continuity will push any holdouts to start buying through the marketplace.

The expansion of subsidies made a difference for many Vermonters, said Strumolo.

According to an analysis by the National Academy for State Health Policy, now 90% of marketplace users receive a subsidy. A quarter of participants pay less than $25 per month for insurance, and across the board, on average, premiums dropped to three-quarters of the previous price.

The extra help also allowed more Vermonters to buy lower-deductible Gold plans, the popularity of which increased 25%, four times the rate of enrollment increase between February 2021 and February 2022.

Vermont officials were very concerned that this improvement would end this year. “We spent a lot of time lobbying for the extension,” Strumolo said. “It was going to create this tremendous affordability cliff for 2023.”

The fix is not permanent. The expansion of benefits will expire in three years. Strumolo said state officials will be looking to Congress or the Vermont Legislature during that time for a more permanent solution.

Who is eligible?

Eligibility for the expanded subsidies has changed even more recently. The “family glitch” was the result of how the Internal Revenue Service interpreted a portion of the Affordable Care Act as it was being implemented. (The IRS is involved because the subsidies are tax credits, though they are most often applied in advance through the marketplace in the form of a reduction in the monthly premium fee.)

A rule change that was approved in October, and that goes into effect before the end of the year, will allow an estimated 14,000 more Vermonters access to the marketplace, according to one 2021 study by the Kaiser Family Foundation.

Since the start of the program, individuals and families have been able to buy through the federal and state marketplaces, and have access to income-based subsidies, if their employer-based coverage is considered either not adequate or if the monthly premium is not affordable. In 2023, the definition of unaffordable for this purpose is more than 9.12% of a household’s monthly income. That is around $482 per month for households with incomes of $63,500, the statewide median in 2022.

However, until now, the employer-offered price used to calculate affordability was the cost of a single-person plan, not the family plan that the employee would actually be purchasing. In general, family plans can cost three to four times as much as individual plans. And now, after nine years, the family cost will be what is considered.

How big are the potential savings?

There is no simple answer to this. That is why state officials are urging families who are struggling to pay employer-based health care to take a second look at the marketplace.

Each situation will be somewhat different, depending on household income, household size, the age of dependent children and whether some household members are eligible for Medicaid or Medicare.

The subsidies are likely to be most impactful for middle-income families making less than $106,000 annually who are now purchasing a family plan through an employer, according to one national study, which suggests savings through the state marketplace for a family of four with an income of $53,000 would be around $3,450 every year.

However, the details make it much more complicated than that.

In Vermont, children under 19 in households of four with income that approaches $90,000 annually are eligible for coverage under Medicaid. (Coverage is available for adults only for households making around $38,000 or less.) So, for example, in a middle-income household in Vermont, an employed adult might be covered by an employer’s insurance and a younger child by Medicaid, while the employee’s partner and an older child (under 26) now are eligible for a subsidy through Vermont Health Connect.

This level of complexity is what makes changing health care plans so daunting for many, Strumolo said. The department has tried to help by providing several online tools to assist. She hopes the prospect of additional savings will prompt people to take the first step: reaching out by phone or creating an account online.